Financial Feudalism

By Dmitry Orlov

March 25, 2015 "ICH"

- Once upon a time—and a fairly long time it

was—most of the thickly settled parts of the

world had something called feudalism. It was

a way of organizing society hierarchically.

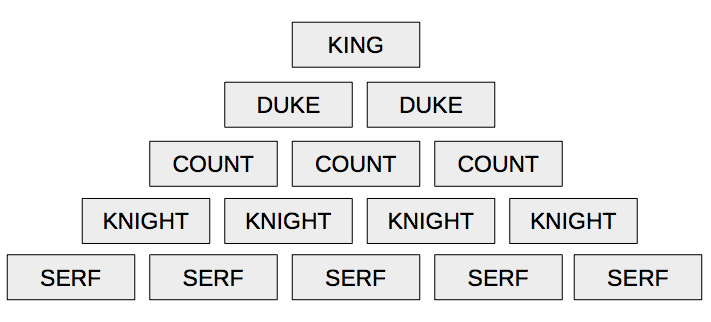

Typically, at the very top there was a

sovereign (king, prince, emperor, pharaoh,

along with some high priests). Below the

sovereign were several ranks of noblemen,

with hereditary titles. Below the noblemen

were commoners, who likewise inherited their

stations in life, be it by being bound to a

piece of land upon which they toiled, or by

being granted the right to engage in a

certain type of production or trade, in case

of craftsmen and merchants. Everybody was

locked into position through permanent

relationships of allegiance, tribute and

customary duties: tribute and customary

duties flowed up through the ranks, while

favors, privileges and protection flowed

down.

It was a remarkably resilient,

self-perpetuating system, based largely on

the use of land and other renewable

resources, all ultimately powered by

sunlight. Wealth was primarily derived from

land and the various uses of land. Here is a

simplified org chart showing the pecking

order of a medieval society.

Feudalism was essentially a steady-state

system. Population pressures were relieved

primarily through emigration, war,

pestilence and, failing all of the above,

periodic famine. Wars of conquest sometimes

opened up temporary new venues for economic

growth, but since land and sunlight are

finite, this amounted to a zero-sum game.

But all of that changed when feudalism was

replaced with capitalism. What made the

change possible was the exploitation of

nonrenewable resources, the most important

of which was energy from burning fossilized

hydrocarbons: first peat and coal, then oil

and natural gas. Suddenly, productive

capacity was decoupled from the availability

of land and sunlight, and could be ramped up

almost, but not quite, ad infinitum, simply

by burning more hydrocarbons. Energy use,

industry and population all started going up

exponentially. A new system of economic

relations was brought into being, based on

money that could be generated at will, in

the form of debt, which could be repaid with

interest using the products of

ever-increasing future production. Compared

with the previous, steady-state system, the

change amounted to a new assumption: that

the future will always be bigger and

richer—rich enough to afford to pay back

both principal and interest.

With this new, capitalistic arrangement, the

old, feudal relationships and customs fell

into disuse, replaced by a new system in

which the ever-richer owners of capital

squared off against increasingly

dispossessed labor. The trade union movement

and collective bargaining allowed labor to

hold its own for a while, but eventually a

number of factors, such as automation and

globalization, undermined the labor

movement, leaving the owners of capital with

all the leverage they could want over a

demoralized surplus population of former

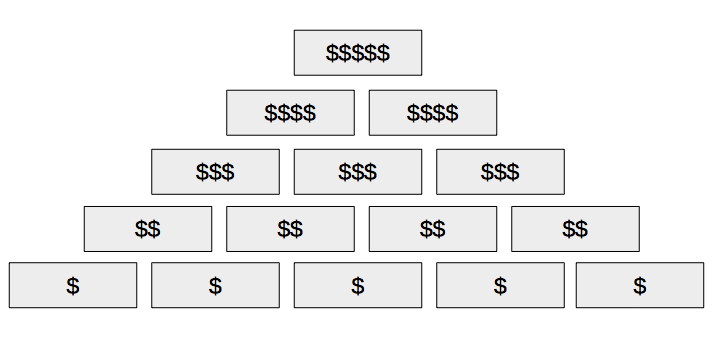

industrial workers. In the meantime, the

owners of capital formed their own

pseudo-aristocracy, but without the titles

or the hereditary duties and privileges.

Their new pecking order was predicated on

just one thing: net worth. How many dollar

signs people have next to their name is all

that's necessary to determine their position

in society.

But eventually almost all the good, local

sources of hydrocarbon-based energy became

depleted, and had to be replaced using

lower-quality, more remote,

harder-to-produce, more expensive ones. This

took a big bite out of economic growth,

because with each passing year more and more

of it had to be plowed right back into

producing the energy needed to simply

sustain, never mind grow, the system. At the

same time, industry produced a lot of

unpleasant byproducts: environmental

pollution and degradation, climate

destabilization and other externalities.

Eventually these started showing up as high

insurance premiums and remediation costs for

natural and man-made disasters, and these

too put a damper on economic growth.

Population growth has its penalties too. You

see, bigger populations translate to bigger

population centers, and research results

show that the bigger the city, the higher is

its energy use per capita. Unlike biological

organisms, where the larger the animal, the

slower is its metabolism, the intensity of

activity needed to sustain a population

center increases along with population.

Observe that in big cities people talk

faster, walk faster, and generally have to

live more intensely and operate on a tighter

schedule just to stay alive. All of this

hectic activity takes energy away from

constructing a bigger, richer future. Yes,

the future may be ever more populous (for

now) but the fastest-growing form of human

settlement on the planet is the urban

slum—lacking in social services, sanitation,

rife with crime and generally unsafe.

What all of this means is that growth is

self-limiting. Next, observe that we have

already reached these limits, and have in

some cases gone far beyond them. The

currently failing fad of hydraulic

fracturing of shale deposits and steaming

oil out of tar sands is indicative of the

advanced state of depletion of fossil fuel

sources. Climate destabilization is

producing ever more violent storms, ever

more severe droughts (California now has

just a year's worth of water left) and is

predicted to wipe out entire countries

because of rising ocean levels, failing

monsoon seasons and dwindling irrigation

water from glacial melt. Pollution has

likewise reached its limits in many areas:

urban smog, be it in Paris, Beijing, Moscow

or Teheran, has become so bad that

industrial activities are being curtailed

simply so that people can breathe.

Radioactivity from the melted-down nuclear

reactors at Fukushima in Japan is showing up

in fish caught on the other side of the

Pacific Ocean.

All of these problems are causing a very

strange thing to happen to money. In the

previous, growth phase of capitalism, money

was borrowed into existence in order to

bring consumption forward and by so doing to

stimulate economic growth. But a few years

ago a threshold was reached in the US, which

was at the time still the epicenter of

global economic activity (since eclipsed by

China), where a unit of new debt produced

less than one unit of economic growth. This

made borrowing from the future with interest

no longer possible.

Whereas before money was borrowed in order

to produce growth, now it had to be

borrowed, in ever-larger amounts, simply to

prevent financial and industrial collapse.

Consequently, interest rates on new debt

were reduced all the way to zero, in

something that came to be known as ZIRP, for

Zero Interest Rate Policy. To make it even

sweeter, central banks accepted the money

they loaned out at 0% interest as deposits,

which earned a tiny bit of interest,

allowing banks to make a profit by doing

absolutely nothing.

Unsurprisingly, doing absolutely nothing

proved to be rather ineffective, and around

the world economies started to shrink. Many

countries resorted to forging their

statistics to paint a rosier picture, but

one statistic that doesn't lie is energy

consumption. It is indicative of the overall

level of economic activity, and it is down

across the entire world. A glut of oil, and

a much lower oil price, is what we are

currently witnessing as a result. Another

indicator that doesn't lie is the Baltic Dry

Index, which tracks the level of shipping

activity, and it has plummeted too.

And so ZIRP set the stage for the latest,

most queer development: interest rates have

started to go negative, both on loans and

deposits. Good bye, ZIRP, hello, NIRP!

Central banks around the world are starting

to make loans at small negative rates of

interest. That's right, certain central

banks now pay certain financial institutions

to borrow money! In the meantime, interest

rates on bank deposits have gone negative as

well: keeping your money in the bank is now

a privilege, for which one must pay.

But interest rates are certainly not

negative for everyone. Access to free money

is a privilege, and those who are privileged

are the bankers, and the industrialists they

fund. Those who have to borrow to finance

housing are less privileged; those who

borrow to pay for education even less so.

Those not privileged at all are those who

are forced to buy food using credit cards,

or take out payday loans to pay rent.

The functions which borrowing once played in

capitalist economies have been all but

abandoned. Once upon a time, the idea was

that access to capital could be obtained

based on a good business plan, and that this

allowed entrepreneurship to flourish and

many new businesses to be formed. Since

anybody, and not just the privileged, could

take out a loan and start a business, this

meant that economic success depended, at

least to some extent, on merit. But now

business formation has gone in reverse, with

many more enterprises going out of business

than are being formed, and social mobility

has become largely a thing of the past. What

is left is a rigidly stratified society,

with privileges dispensed based on

hereditary wealth: those at the top get paid

to borrow, and get to surf on a wave of free

money, while those at the bottom are driven

ever further into debt servitude and

destitution.

Can NIRP underpin a new feudalism? It

certainly cannot reverse the downward slide,

because the factors that are putting limits

on growth are not amenable to financial

manipulation, being physical in nature. You

see, no amount of free money can make new

natural resources spring into existence.

What it can do, however, is freeze the

social hierarchy among the owners of

capital—for a while, but not forever.

Everywhere you care to look, the

ever-shrinking economy eventually results in

populist revolt, war and national

bankruptcy, and these cause money to stop

working in a number of ways. There is

usually devaluation, bank failures,

inability to finance imports, and the demise

of pensions and of the public sector. The

desire to survive causes people to focus on

getting direct access to physical resources,

distributing them among friends and family.

In turn, this causes market mechanisms to

become extremely opaque and distorted, and

often to stop functioning altogether. Under

these circumstances, how many dollar signs

someone has next to their name becomes

rather a moot point, and we should expect

the social hierarchy among the owners of

capital to become unstable and capsize. A

few among them have the talents to become

warlords, and these few fleece the rest out

of existence. But overall, in a situation

where financial institutions have failed,

where factories and other enterprises are no

longer functioning, and where real estate

holdings have been overrun by marauding mobs

and/or invaded by squatters, one's net worth

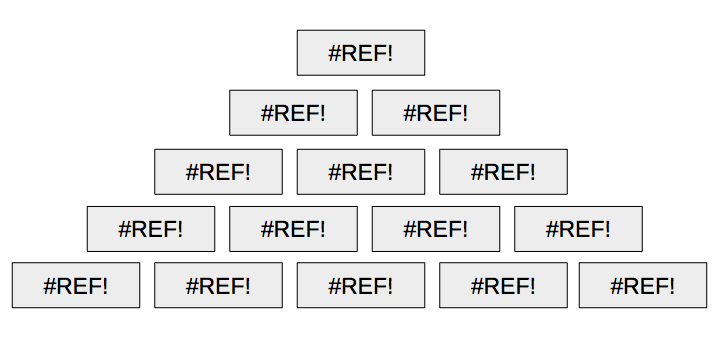

becomes rather difficult to compute. And so

we should expect the org chart of the

post-capitalist society, in spreadsheet

terms, to look like this. (“#REF!” is what

Excel displays when it encounters an invalid

cell reference in a formula.)

A good, precise term for this state of

affairs is “anarchy.” Once a new, low level

of steady-state subsistence is reached, the

process of aristocratic formation can begin

anew. But unless a new source of cheap

fossil fuels is somehow magically

discovered, this process would have to

proceed along the traditional, feudal lines.

Dmitry

Orlov is a Russian-American engineer and a

writer on subjects related to "potential

economic, ecological and political decline

and collapse in the United States,"

something he has called “permanent crisis”.

http://cluborlov.blogspot.com

|

Click for

Spanish,

German,

Dutch,

Danish,

French,

translation- Note-

Translation may take a

moment to load.

What's your response?

-

Scroll down to add / read comments

|

|

Support Information Clearing House

|

|

|

Please

read our

Comment Policy

before posting -

It is unacceptable to slander, smear or engage in personal attacks on authors of articles posted on ICH.

Those engaging in that behavior will be banned from the comment section.

|

| |

|